Chapter One: Introduction to Book-keeping

Introduction

Book-keeping equips students with essential skills and knowledge vital for their future careers. When students master Book-keeping principles and concepts, they will gain a solid foundation for understanding financial transactions and record them accurately. A strong understanding of Book-keeping knowledge and skills empowers students to contribute effectively to both financial success in business arena and in managing personal financial matters. In this chapter, you will learn concept of Book-keeping by focusing on the origin, meaning, scope, purpose, types of Book-keeping methods or systems, relationship with other disciplines and basic terms used in Book-keeping. The competencies developed will enable you to appreciate the importance of keeping business financial transactions and have ability to negotiate and reason effectively during business deals.

Think

On the ways in which your parents or guardians are keeping records of their income and expenses.

Concept of Book-keeping

One of the common occupations that form an important part of day-to-day income generation in any country is business. Although, many businesses are also conducted by large companies both locally and internationally, a significant number of people in business are involved in small businesses. We interact with small businesses every day in the process of buying our daily needs. Typical small businesses include hawkers, vegetable vendors, street retail shops, shoe shining, newspaper vending, salon businesses (hair dressers), artisans and many others. All these businesses make different financial transactions, involving buying inputs or materials, doing some processing, and selling their goods or delivering services.

Book-keeping is a necessary process for any business enterprise. Business operators or owners without the proper knowledge of Book-keeping will somehow unknowingly apply Book-keeping principles in order to achieve various objectives of their businesses.

Take an example of Mrs Chaza who starts a food vending business by the name of Swahili-bites. This business operates near Jenga-afya Secondary School in Maruku. The business will need equipment like cookers, pans and serving utensils. It will also need some furniture like benches, tables and cupboards. It will buy raw food and cook it for sale. To ensure that the food business runs successfully, Mrs Chaza might be required to do the following:

- Hire some cooks and service attendants,

- Supervise cooking activities,

- Sell food,

- Receive cash from sales made, and

- Record credit sales (in case some food is sold on credit).

All these activities will involve movement of money. Eventually, Mrs Chaza would need to evaluate whether the business is achieving its objectives. One of the likely objectives is to make a profit from such operations. This means that Mrs Chaza will need to calculate whether her business has generated a profit or not. To be able to determine the profit or a loss, some calculations will have to be done by comparing the sales (revenue) made from selling food against the costs of materials and services used. To do this, there would be a need to keep records of money paid on each material and services, as well as money received from selling food to customers. Simply put, the process of keeping records of money spent on each material and service as well as money received from selling goods to customers is what is known as "Book-keeping".

Origin of Book-keeping

The origin of Book-keeping can be traced back to the ancient civilisations like Sumeria and Egypt. These societies developed systems to record and track transactions and goods exchanged. Overtime, Book-keeping principles advanced to various techniques through contributions from Greeks and Romans entrepreneurs. In the medieval period, Luca Pacioli in 1494 played a significant role in promoting double entry Book-keeping system. This introduction was a significant development that revolutionised the field of Book-keeping. Since then, Book-keeping has continued to evolve, adapting to changing economic systems and technological advancements. As we speak, Book-keeping remains a vital part of accounting and financial management, ensuring maintenance of records, facilitating financial reporting, analysis, and maintaining transparency and accountability in financial affairs.

Meaning of Book-keeping

Book-keeping is an important part of the accounting process. It plays an important role in the early stages in the accounting process. As explained earlier, Book-keeping can be defined as the art of recording business financial transactions in the books of accounts in an orderly manner. In principle, every transaction has to be recorded in a systematic manner. Such recording includes proper classification according to the nature of the transaction. The end result of Book-keeping is to have net figures or balances in the ledger accounts. This will help to determine a profit or a loss and the financial position of the business. Book-keeping also helps in the management of credit dealings, proper control of the business and appropriate computation of taxes. Hence, Book-keeping is the systematic recording, organising and tracking of financial transactions and activities within a business.

Activity 1.1

Visit any nearby food vendors or mobile money service shops and investigate various activities, involving keeping financial records. Thereafter, read textbooks or online reliable sources. Compare what you have seen and read, then write down your understanding about the concept of Book-keeping in your own words.

Scope of Book-keeping

The process of Book-keeping covers the recording, classification, organisation and maintenance of records of financial transactions. It plays central role in providing accurate financial information for decision making, legal and regulatory compliance and financial analysis within a business.

Purpose of Book-keeping

The purpose of Book-keeping is to enable business to record and track the financial transactions of an enterprise or business activities. Book-keeping provides clear and organised records of business financial transactions, including sales, purchases, consumption, payments and receipts. The specific purposes of Book-keeping include:

- Financial records: Book-keeping ensures all financial records are properly documented and easily accessible when needed. It provides a comprehensive record of financial transactions, which helps in maintaining a clear and accurate account of the enterprise's financial activities.

- Compliance and legal requirements: Book-keeping plays a crucial role in fulfilling legal and regulatory obligations. Organised and appropriate financial records are necessary for preparing tax returns and, meeting financial reporting requirements.

- Financial management: Book-keeping provides information for effective financial management. It enables businesses to track expenses, monitor cash flow, and evaluate financial resources. By having up-to-date financial records, an enterprise can make informed decisions regarding investment, budgeting and resource allocation.

- Facilitating business decision making: Book-keeping provides insights into revenue generation, cost management, and profitability. The information helps in making sound business decisions.

Management with accurate financial data can analyse different aspects of the business, identify areas for improvement, and make strategic decisions to drive business growth.

Importance of Book-keeping

Book-keeping is important to business owners and other parties outside the enterprise in the following ways:

Determination of profits or losses

Book-keeping helps a business to determine whether it is making a profit or a loss. This is possible because Book-keeping helps the enterprise to keep complete, accurate and up-to-date financial records that are used in preparing financial statements. Take an example of Mrs Chaza on page 2 Book-keeping assists the business to calculate profits or losses made for any period from the food vending business.

Knowledge of credit transactions

Many businesses are conducted on both cash and credit basis. For example, Mrs Chaza, would sell most of its food for cash, but she would occasionally sell to some customers on credit. Similarly, it is possible that Mrs Chaza buys some of its raw foods on credit from the market. In practice, many businesses have a significant volume of transactions conducted on credit. Book-keeping helps the enterprises to maintain appropriate records of their credit transactions and know the amount due from each of its debtors and the amount owing to each of its creditors. Such records can systematically be kept following Book-keeping principles.

Debtor: This is a customer who has bought goods on credit from business and promises to pay at a later date.

Creditor: This is a supplier who sold goods or provided service on credit to the business for payment to be made at a later date.

Control of business

To have an effective control of a business, the owner of the business needs to keep proper records of his or her financial matters. These records, in the long run, help the owner to decide on matters such as expansion or reduction of the business. If Mrs Chaza sells breakfast, lunch and dinner; appropriate record keeping may assist in deciding on the extent of efforts to dedicate to each of the menus. Additionally, in case the food is sold from more than one location or centre; Book-keeping may suggest whether the volume in one or another centre may need to be expanded or reduced according to the sales records. Book-keeping can also help the proprietor to see whether there are possible incidences where money, foodstuff or materials have been stolen or misused. This can be useful in making a decision on the corrective measures to be taken where necessary.

Determination of business's financial position

Book-keeping helps the owner to determine the financial position of his or her enterprise. It enables him or her to understand the value of assets, liabilities, and the amount of capital contributed by the owner. This can be useful in establishing whether the business has grown or not. Knowing the financial position of a business can also assist in applying for a loan or other form of credit for expanding its operations.

Tax assessment

Tax authorities such as the Tanzania Revenue Authority (TRA) and Zanzibar Revenue Authority (ZRA) need to receive and examine the books of accounts of every enterprise operating in the United Republic of Tanzania. This is important in calculating the amount of tax that should be paid by the enterprises. Tax laws in Tanzania use self-assessment system, where for some taxes the taxpayer is required to make own calculation of tax payable. Thus, proper keeping of financial records helps both the owner and tax authorities to assess the amount of tax payable. Tax laws in Tanzania also penalise businesses that do not maintain financial documents and records properly. Book-keeping therefore, may help the business save money that would otherwise be paid as penalties for not maintaining financial records.

Figure 1.1: Logos of key organs responsible for revenue administration in Tanzania

(a) Tanzania Revenue Authority

(b) Zanzibar Revenue Authority

Accounting process or accounting cycle

The determination of a profit or a loss, together with other objectives, is done through the preparation of financial statements. The entire process that businesses undertake to prepare financial statements from accounting records is known as the accounting cycle. The accounting cycle involves eight stages, and Book-keeping plays an active role in the first seven. The stages in the accounting cycle are summarised as follows:

- Identifying transactions using the source documents,

- Recording the transactions in the books of prime entry,

- Posting transactions to the ledger accounts,

- Extracting the trial balance,

- Making adjusting entries and correction of errors,

- Extracting the adjusted trial balance,

- Preparing the financial statements, and

- Analysing and interpreting the financial statements.

Identifying transactions and recording in source documents

This is the first stage in the accounting process where financial transactions are identified and evidenced through source documents such as receipts, payment vouchers, invoices, cheques, debit note and credit note. For a transaction to be identified and evidenced, it must be of a financial value and it must affect at least two items of the accounting equation.

Recording the transactions in the books of prime entry

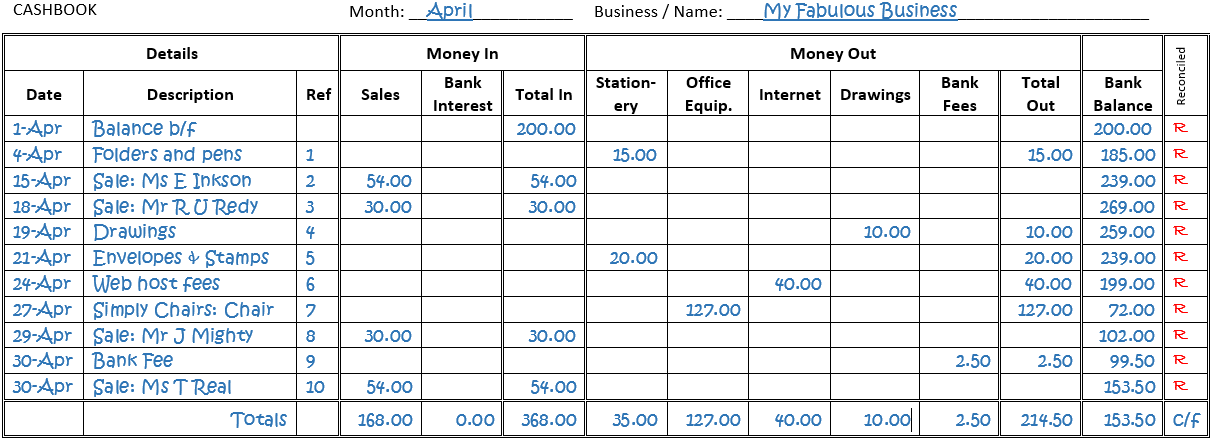

The second stage is to record such transactions in the books of prime entry, which are also known as books of original entry. The transaction is initially recorded in these books before it is recorded or posted anywhere else. This book will focus on six types of books of prime entry, namely a sales journal, a purchases journal, a sales returns journal, a purchase returns journal, a general journal, and a cash book.

Posting transactions to the ledger accounts

The third stage in the accounting cycle is posting transactions to the ledger accounts. This process involves the posting of entries that were initially recorded in the books of prime entry to the ledger accounts. The posting of entries to the respective ledger accounts is done by following the double entry system of Book-keeping.

Extracting the trial balance

The fourth stage in the accounting cycle is the extraction of the trial balance. The trial balance is a list prepared at a specific date showing net figures or balances of all general ledger accounts. The account balances extracted from the general ledger are listed in the debit and credit columns of the trial balance. The debit and credit columns must balance. The trial balance is usually prepared to check the arithmetical accuracy of double entries made to the ledger accounts, and it acts as a compiled list of balances for use in the preparation of financial statements.

Account: This is a summarised record of business transactions. It can be presented on a page of a ledger book.

Debit and Credit: These are two terms which are used in describing the two sides of an account, that is, the left-hand side (Debit) and the right-hand side (Credit).

Double entry: This is the system or principle of Book-keeping whereby each business transaction is recorded in the book of accounts.

Making adjusting entries and correction of errors

A trial balance is expected to reveal some errors made when transactions are first entered in the books of prime entry or when double entry is done in the ledger. These errors need to be corrected. This is a process that goes together with making any necessary adjustments of the balances before the preparation of financial statements.

Extracting the adjusted trial balance

After correcting the errors and making adjusting entries, the adjusted trial balance will need to be prepared. This is the one that has balances that are used in the preparation of financial statements.

Preparing the financial statements

Financial statements are prepared using figures extracted from the adjusted trial balance. The aim of preparing the financial statements is to know the performance, financial position and cash flows of the enterprise. This includes determining whether the enterprise is making profits or losses (usually done through preparing an income statement) and to show the financial wealth of the enterprise. This is done through the statement of financial position.

Analysing and interpreting the financial statements

The financial statements need to be analysed and interpreted to assess the performance of the enterprise. This is done in comparison with other enterprises, as well as the progress made from one period to another. One of the tools used for analysing financial statements is ratio analysis. Analysed financial information is useful to several users such as owners, lenders and creditors in making informed decision.

Types of Book-keeping methods/systems

Modern Book-keeping uses double entry system. However, some businesses still find it adequate to use a single entry system. The following are the two systems of Book-keeping:

Double-entry Book-keeping

Double-entry Book-keeping is a more comprehensive and widely used method that provides a more accurate and detailed representation of business's financial transactions. It follows the principle that every transaction has equal and opposite effects on at least two accounts. Each transaction is recorded with a debit entry in one account and an equal credit entry in another. This method maintains a system of accounts, including assets, liabilities, equity, revenue, and expenses. Double-entry book-keeping ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced and allows for the preparation of accurate financial statements such as statement of financial position and income statements.

Single-entry Book-keeping

Single-entry book-keeping is a simple and straightforward method primarily used by small businesses or individuals with relatively few repetitive and uncomplicated financial transactions. In this method, only a single entry is made for each transaction, typically in a revenue or expense journal or a cash book. It records income and expenses, but it does not track individual accounts for assets and liabilities. Single-entry book-keeping is used for basic record-keeping purposes such as tracking cash receipts and payments.

These two types of Book-keeping methods differ in complexity and the level of financial details they provide. While single-entry Book-keeping is suitable for small businesses with straightforward transactions, double-entry Book-keeping is the standard method used by most businesses due to its accuracy, reliability, and ability to provide a comprehensive financial overview.

Common terms used in Book-keeping

Book-keeping includes the recording and organisation of financial transactions in a systematic manner. The recording and organisations of financial inspections involve the use of various terms. These terms provide the basic understanding of the concepts and terminologies used in Book-keeping. The following are some basic terms used in book-keeping:

| Term | Definition |

|---|---|

| Assets | Resources controlled by a business owner that have economic benefits to the business. These include cash, inventory, equipment, and property. |

| Liabilities | Debts or obligations of a business to external parties, such as loans, trade and other payables, and accrued expenses. The business has duty to settle such obligations through economic resources, for example cash. |

| Expenses | Costs incurred by a business in the process of generating revenue, including salaries, rent, utilities, supplies, and other operating expenses. |

| Debit entry | An entry on the left side of an account, representing an increase in assets or expenses or a decrease in liabilities or revenue. |

| Credit entry | An entry on the right side of an account, representing an increase in liabilities, or revenue or a decrease in assets or expenses. |

| Double-entry | A system of book-keeping that records each financial transaction with equal and opposite entries on two different accounts. |

| Ledger | is a book or digital record in which financial transactions are recorded. It is a fundamental element of book-keeping used in tracking, organising, and summarising financial information. |

| Journal | The book or electronic record where financial transactions are initially recorded in chronological order. |

| Debtor | This term refers to a customer who buys goods or services from an enterprise on credit. Thus, a debtor is a person who owes money to the business. He or she has an obligation to the business. The amount receivable from the debtors of the enterprise is an asset to such enterprise and is treated as a current asset in the statement of financial position. Another name for debtor is accounts receivable. |

| Creditor | This refers to a person who sells goods or renders services on credit to an enterprise. Therefore, a creditor is a person to whom the enterprise owes money. The amount payable to creditors of the enterprise is a liability to that enterprise and is treated as a current liability in the statement of a financial position. Another name for creditor is accounts payable. |

| Trade receivables | This refers to money owed to a business by its customers for goods or services sold on credit. |

| Other receivables | This refers to amounts receivable from persons other than those resulting from credited sales of goods or services to customers. An example of other receivables are the ones resulting from the business lending money to its employees. |

| Trade payables | This refers to money owed by a business to its creditors or suppliers for goods or services purchased on credit. |

| Other payables | This refers to amounts payable to persons that result from transactions with the business other than purchases of goods for resale. An example is where the business buys a non-current asset on credit. |

| General ledger | This refers to the central repository of all financial transactions recorded by a business. It is categorised by accounts such as cash, accounts payable, and accounts receivable. |

| Trial balance | It is a list of all general ledger accounts and their balances. It checks whether debits equal to credits and to detect any errors before preparing financial statements. |

| Revenue | The terms refers to income generated by a business through its primary operations, such as sales of goods or services. |

| Depreciation | This refers to the systematic allocation of the cost of a long-term asset over its useful life to match such cost with the revenue generated by the asset over its life. |

| Cashflow | This refers to the movement of cash into and out of a business over a specific period. Cashflows can either be cash inflows or cash outflows. |

| Business | This refers to any legal activity undertaken with the aim of achieving a particular objective, such as making profits, and reaching a targeted service level. Examples of business include farming, a restaurant, a salon and a kiosk. |

| Capital | It is the amount of money or money's worth provided by the owner to start an enterprise or to expand it. The money contributed by the owner can be used to finance business operations or grow and expand the business. |

| A sole proprietor | A sole proprietor is the owner of the enterprise who provides capital to start or expand the enterprise alone. The sole proprietorship is the form of business enterprises that is owned by one person. In most cases, sole proprietorship is a family business and is the easiest type of business to establish and operate because it is not highly regulated by the government. |

| Goods | These are items bought and sold by the proprietor and they have the characteristics of being seen and touched. Goods are sold by business people to satisfy the needs of customers. Examples of goods include pens and exercise books for a stationeries business, food for restaurant business and cement for a hardware business. |

| Services | These are activities performed by the enterprise in the course of business that does not involve itself in selling physical goods. Examples of services offered by different enterprises are hairdressing, drama shows, advertising and training. It should be noted that some businesses deal with both goods and services. |

| Profit | Result achieved by the business when revenues are greater than expenses for a particular period or activity. In other words, profit is the excess of revenue over expenses for a particular period or activity. |

| Loss | A business is said to make loss when expenses are greater than revenues for a particular period or activity. A loss is not desired by any enterprise because it reduces the amount of capital of such enterprise. |

| Transaction | A transaction is a business event that has monetary impact on business financial statements, and is recorded as an entry in the business' accounting records. It also refers to the movement of money or money's worth between two or more parties. For example, Juma paid Paula TZS 20,000 to buy a pair of shoes. This is a transaction because TZS 20,000 have been transferred from Juma to Paula and at the same time, the pair of shoes has been transferred from Paula to Juma. |

Activity 1.2

Sakara is a businessman who does not have a Book-keeping knowledge and has been running a restaurant for years. His friend, Kapesa told Sakara about you, specifying that you are a student studying Book-keeping at Busara Secondary School. She informs Sakara that you can explain some of the basic concepts of Book-keeping to him. You are approached by Sakara to clarify for about Book-keeping and the importance of using Book-keeping in his business. Prepare a brief note that will guide your talk to Sakara in relation to his concerns.

Relationship between Book-keeping and other disciplines

Book-keeping supports operationalisation of other disciplines. The knowledge and skills acquired in Book-keeping are also applicable in different subject areas covered in the Ordinary Secondary Education Curriculum and beyond. The relationship that exists between Book-keeping and some other disciplines is explained as follows:

Accountancy

Book-keeping lays down the foundation of the Accountancy subject. It deals with recording and posting entries to various ledgers that are used by accountants to analyse, interpret and make informed decisions about the business. Accountants produce reports popularly known as financial statements. These financial statements are prepared using balances that are generated from the ledgers, which are prepared by book keepers. Financial information is important for business management, investments, tax assessment, and government regulations activities. Therefore, without the knowledge of Book-keeping, it would be difficult, for accountants to prepare and analyse financial statements.

Business studies

Book-keeping provides skills for preparing manufacturing accounts and how to accumulate various costs which are related to commercial activities. The relationship between Business Studies and Book-keeping lies in their business activities which result in financial generation. Business Studies provide a broader understanding of the overall business environment and operations, while book-keeping is a systematic recording of financial transactions gained from business activities.

Economics

Book-keeping knowledge allows students of Economics to calculate real costs. Also, Book-keeping develop skills for maintaining economics records, calculating national income, performing cost analysis and production costs. Both disciplines contribute to the effective financial management and informed economic decision-making.

Home Economics

Book-keeping supports Home Economics by providing a system to financial record-keeping, budgeting, expenses tracking, financial planning, tax preparation and decision-making within household. It helps individuals and families to effectively manage their resources, making informed financial choices and achieve their financial goals.

Computer Science

Book-keeping and computer science relate through the preparation and analysing of financial statements. Computer has automated tools that enhance financial record-keeping, data analysis, security measures, and reporting processes. Computer scientists contribute by creating accounting software, ensuring data integrity, implementing security measures, utilising artificial intelligence to prepare financial statements and reports.

Agriculture

Book-keeping is closely tied to agriculture through financial tracking, cost analysis, budgeting, financial planning, inventory management, tax compliance, and financial analysis. It helps farmers to maintain financial records, assess profitability, optimise resource allocation, comply with tax obligations, and make informed decisions to achieve sustainable and profitable agricultural operations. Also, agriculture deals with farming management that requires the preparation of farm records and farm accounting. This includes depreciating the value of farming equipment and keeping inventories of farm produce. The analysis of farming accounts is done after preparing their books of accounts. In order to do that, one needs to have Book-keeping knowledge and skills.

Exercise 1.1

- What do you understand by Book-keeping? Explain its importance and scope.

- What are the basic concepts of Book-keeping? Why is it important for a business person to use Book-keeping systems to keep financial records?

Summary

Book-keeping is a fundamental concept in financial management, involving the systematic recording, organising, and summarising of information about financial transactions. Its origins can be traced back to ancient civilisations where basic record-keeping practices were employed. Today, Book-keeping has evolved into a structured discipline with defined principles and techniques.

The purpose of Book-keeping is to provide a basis for a clear and accurate representation of business's financial activities. It encompasses tasks such as recording transactions, classifying them into appropriate accounts, and generating financial statements. Book-keeping plays a vital role in supporting decision-making by providing insights into cashflows, assets, liabilities, revenue, and expenses. It also ensures compliance with legal and regulatory requirements, facilitates financial analysis, and enhances transparency and accountability.

Within the realm of Book-keeping, various terms are commonly used in describing key concepts. These include assets (the resources owned by a business), liabilities (the debts or obligations), revenue (the income generated), expenses (the costs incurred), accounts receivable (amounts owed to the business by its customers), accounts payable (amounts owed by the business to its suppliers), cashflows (the movement of cash), journals (chronological records of transactions), ledgers (individual account records), and financial statements (such as statement of financial position and income statements). Familiarity with these terms is crucial for accurate record-keeping and effective financial management.

Revision exercise 1

- Explain how the origin and historical development of Book-keeping as a concept has influenced modern accounting practices.

- Describe the scope of Book-keeping and its role within the broader field of financial management.

- Explain the purposes of Book-keeping and its contribution to financial decision-making.

- Describe types of financial transactions covered in Book-keeping.

- Provide a brief overview of Book-keeping and highlight its importance in managing financial records.

- Identify and describe the eight stages in the accounting cycle, explaining the purpose and activities involved in each stage.

Chapter Two: Basic Principles of Book-keeping

Introduction

The basic principles of Book-keeping provide students with the necessary skills and knowledge of maintaining appropriate financial records, complying with regulations, and making informed decisions. These principles enable students to pursue various career paths in the field of accounting and finance. In this chapter, you will learn accounting principles and assumptions, single entry and double entry system of Book-keeping. The competencies developed will enable you to use basic accounting principles in recording and preparing financial statements.

Think

What would it be if there were no basic principles and guidelines in Book-keeping.

Accounting Principles and Assumptions

In the world of Book-keeping, the recording and presenting of financial information is guided by book-keeping principles. Book-keeping principles refer to the various frameworks which guide the practice of accounting. These principles guide the procedures and practices in measuring, recording, and communicating financial information to different users. Book-keeping principles are concerned with appropriately presenting an enterprise's financial information. Accounting concepts are concerned with guiding recording of transactions and preparations of financial statements. In this chapter, some accounting principles and concepts shall be discussed in detail.

Monetary Unit Principle

This is also known as the unit of measurement principle. It states that financial transactions should be recorded and reported using a common unit of measurement in monetary terms. Most countries would require that financial statements are presented in their local currency, for example, Tanzanian shillings (TZS).

The monetary measurement principle states that only transactions or events that can be expressed in monetary terms should be included in the accounting records. This principle implies that only measurable and quantifiable economic events should be recognised and reported in the financial statements. Items that can not be quantified in monetary terms are not recorded in financial statements. This is because they lack a reliable monetary value. For example, the skills of employees and reputation of an enterprise. This principle along with other accounting principles and concepts, provide a framework for preparing financial statements that are comparable. It ensures that financial information is recorded, measured, and reported consistently, allowing for meaningful analysis and decision-making.

Going Concern Principle

The going concern principle, also known as the continuity assumption, assumes that a business will continue its operations beyond a reasonable length of time it will not be forced to liquidate or cease operations in the foreseeable future. This principle underlies the preparation of financial statements and the basis for valuing assets and liabilities. The going concern principle assumes that the business can realise its assets, settle its liabilities, and fulfil its commitments in the normal course of operations. As a result, assets are generally recorded at their historical cost and are not immediately adjusted to their liquidation or forced-sale values, unless evidence suggests that it will cease to operate in the near future (within the next 12 months).

The going concern principle is significant in assessing the financial health and viability of a business. Financial statements prepared using this principle provide information to users about the enterprise's ability to meet its financial obligations, continue operations, and generate profits in the long term. However, if circumstances arise that raise doubts about the business's ability to continue as a going concern, such as significant financial difficulties or legal issues, the going concern principle may be questioned. In such cases, additional disclosures or adjustments may be required to reflect the potential impact on the financial statements.

The going concern principle ensures that financial statements reflect the assumption of business continuity. It also allows stakeholders to make informed decisions based on the assumption that the enterprise will continue its operations in the foreseeable future.

Time Period Principle

The time period principle, also known as the periodicity concept, suggests that the financial activities of a business should be divided into specific and meaningful time periods for reporting purposes. This principle allows for the systematic and regular preparation of financial statements, providing timely and relevant information to users.

Under this principle, the financial year is divided into shorter periods, such as months, quarters or years, depending on the reporting requirements and industry practices. Financial transactions and events are recorded and summarised within these designated time periods, enabling the preparation of interim and annual financial statements. The time period principle helps to facilitate the analysis and comparison of financial information over different periods. By breaking down the financial activities into uniform time intervals, it allows stakeholders to assess the business's performance, identify trends, and make informed decisions based on up-to-date information.

Matching Principle

This is a fundamental accounting principle that guides the recognition of expenses in financial statements. It states that expenses should be recognised and recorded in the same accounting period in which they are incurred to generate revenue. The principle aims to achieve a proper matching of expenses with the revenues earned during a specific period. This provides a more accurate representation of the business's financial performance.

According to the matching principle:

- Expenses should be recognised when the related revenue is recognised: When a business earns revenue from the sale of goods or the provision of services, it should also recognize the expenses directly associated with generation of that revenue in the same period. This ensures that the costs incurred to generate revenue are properly matched with the revenue in the financial statements.

- Expenses should be recognised in a systematic and rational manner: The matching principle requires expenses to be recognised in a logical and consistent manner over the accounting periods. It discourages the recognition of expenses only when payment is made or received.

By following the matching principle, businesses can provide more accurate meaningful measure of performance. It allows users of financial statements to assess the profitability and financial performance of a business by matching the expenses directly to the revenues they helped to generate.

Example 2.1

An enterprise sells products in February but had incurred the associated manufacturing costs in November. The matching principle requires matching the costs incurred in November on manufacturing the goods, with the revenue generated in February when the products are sold.

Revenue Recognition Principle

This is a fundamental accounting principle that determines when and how revenue should be recognised or recorded in the financial statements. It provides guidance on when to recognize revenue and how to measure it. It also ensures that revenue is reported accurately and in the appropriate period. According to the revenue recognition principle, revenue should be recognised when it is both realised or realisable and earned. This occurs when the following criteria are met:

- Identification of the contract: There should be a legally enforceable agreement between the seller and the buyer, outlining the rights and obligations of both parties.

- Delivery of goods or services: The seller has transferred control of the goods or services to the buyer.

- Determination of the transaction price: The transaction price is determined and can be reasonably estimated. It includes consideration received or expected to be received from the buyer in exchange for the goods or services.

- Collectability probability: It is probable that the seller will collect the amount he or she is entitled to receive from the buyer.

Once these criteria are met, revenue should be recognised in the accounting records. The amount recognised is typically the fair value of the consideration received or receivable in exchange for the goods or services provided. The revenue can be recognised at a point in time (for example, when the goods are delivered) or over time (for example, as services are performed). It is important to note that specific industries or transactions may have additional guidance or standards for revenue recognition, such as long-term construction contracts or software sales. These industry-specific rules may provide further criteria or guidelines to determine when revenue should be recognised.

In summary, the revenue recognition principle insists on recognising revenue in the books when activities involving sale of goods or service have reasonably been performed, amount is known and has been collected or is reasonably expected to be collected.

Accrual Basis Accounting Principle

This is the method of recording and reporting financial transactions based on when they occur, regardless of the timing of cash inflows or outflows. In the accrual basis, revenue is recognised when it is earned, and expenses are recognised when they are incurred, regardless of when cash is received or paid. The key principles of the accrual basis of accounting include:

- Revenue recognition: Revenue is recognised when it is earned, meaning when goods are delivered, services are rendered, or contractual obligations are fulfilled. It is recognised even if payment is not received at that time. This principle ensures that revenue is matched with the period in which it is earned. This provides a more accurate depiction of an enterprise's financial performance.

- Expense recognition: Expenses are recognised when they are incurred, meaning when goods or services are received or consumed, regardless of when payment is made. This principle ensures that expenses are matched with the related revenues or the period in which they contribute in generating revenue.

Activity 2.1

Imagine you are in charge of tracking money for a small shop. Can you tell your friend about a time when the shop spent or earned money? Then, explain how you would write it down in the shop's money records. You need to write down two things: one for the money that goes out and one for the money that comes in. Can you also explain why you are writing those things down?

Materiality Principle

The materiality principle states that financial information should be reported and disclosed if it has the potential to influence the decision-making of users of the financial statements. Materiality is determined by the nature and amount of an item or event. If an item or event is significant to impact the assessment or evaluation of a business's financial position, performance, or cash flows, it should be disclosed in the financial statements. The materiality principle recognises that not all financial information is of equal importance. It allows accountants to focus on reporting information that is relevant and significant, while avoiding excessive detail that may not affect the decision-making process. Allowing excessive details may crowd the important information that would be the focus of the users of accounting information. This principle encourages someone to exercise professional judgment in determining material information that requires clear and transparent disclosure in the financial statements. Information is therefore material if its inclusion or omission in the financial statements can affect the decision of the users of financial statements.

The materiality principle acknowledges that financial statements should present a true and fair view of a business's financial position and performance. It enables users to make informed decisions based on the significant factors affecting the business's financial outcomes. Applying the materiality principle requires someone to exercise professional judgment, considering both quantitative and qualitative factors. Accountants must consider the impact of an item or event on the financial statements and the potential influence it may have on the decisions of users.

By considering materiality principle, financial statements can provide a balance between the need for comprehensive and accurate reporting and the practicality of focusing on information that is most relevant and significant to the users of the financial statements.

Historical Cost Principle

Historical cost accounting is an accounting principle that states that, assets should be recorded and reported at their original cost when acquired by an enterprise. According to this principle, the initial cost of an asset represents its value, regardless of any changes in market value over time. In this principle, when an enterprise acquires an asset, it is recorded on the financial position statement (balance sheet) at the price paid to acquire or produce the asset. This cost includes the purchase price and any additional costs incurred to bring the asset to its present condition and location, such as transportation costs and installation fees.

The rationale behind the historical cost principle is to provide a reliable and objective basis for financial reporting. By using the original cost of an asset, financial statements reflect the actual resources expended by the enterprise at the time of acquisition. This principle promotes consistency and comparability in financial statements. It avoids general estimates of an asset's value and prevents manipulation of reported figures based on market fluctuations.

However, critics argue that the historical cost principle may not provide a relevant and accurate representation of an asset's true value, particularly for long-lived assets like property, plant, and equipment. Over time, the market value of assets may change due to factors such as inflation, technological advancements, or changes in market conditions. Some alternative valuation methods, such as fair value accounting, attempt to address these limitations by valuing assets at their current market value. Despite its limitations, the historical cost principle remains widely used in financial reporting, especially for assets that do not have determined market values. It provides a conservative approach to valuing assets and is considered a fundamental principle in traditional accounting practices. Historical cost principle is in line with the going concern principle.

Consistency Principle

This principle states that once an accounting method or principle has been chosen and applied, it should be consistently used for similar transactions and events in subsequent periods. In other words, an entity should not change its accounting methods or principles arbitrarily from one period to another, as it can create confusion and make it difficult to compare financial information across different periods.

Consistency in accounting allows for better comparability of financial statements, enabling users to make meaningful comparisons and assessments of an entity's financial performance and position over time. If a change in accounting methods or principles is deemed necessary, it should be accompanied by proper disclosure and justification, typically in the notes to the financial statements. It is important to note that the consistency principle does not mean that accounting methods cannot be changed or updated. Changes in accounting standards, regulations, or circumstances may require adjustments to accounting methods. However, any changes should be made with careful consideration and with the aim of improving the relevance and reliability of financial information.

Prudence/Conservatism Principle

Prudence, also known as the conservatism principle, is an important concept in Book-keeping and accounting. It suggests that when faced with uncertainty or doubt, accountants should exercise caution and choose the option that is more conservative or prudent. In other words, it is better to make mistakes on the side of understating assets and revenues or overstating liabilities and expenses rather than overstating assets and revenues or understating liabilities and expenses.

The prudence principle helps to ensure that financial statements are not too optimistic or misleading. It encourages a conservative approach to reporting financial information, which can help to prevent overstatement of assets or income and mitigate the risk of financial misstatements or manipulation. By recognising potential losses or risks more quickly and being cautious in revenue recognition, the prudence principle promotes a more realistic and reliable representation of an entity's financial position and performance.

It is important to note that the prudence principle should be applied judiciously and should not be used as a justification for intentionally understating assets or income or overstating liabilities or expenses. The principle aims to strike a balance between caution and providing a true and fair view of an entity's financial position and performance.

Dual Aspect or the Duality Principle

In Book-keeping, the dual aspect or duality principle is a fundamental concept in accounting that forms the basis for the double-entry Book-keeping system. According to the duality principle, every financial transaction has two offsetting effects. Each transaction affects at least two accounts, with equal effects that cancel each other. This principle recognises that every transaction involves a give-and-take relationship. This is the foundation of the double entry principle that has become a strong principle applied in the field of accounting.

Double Entry System

This is an accounting system whose application promotes accuracy and reliability in recording financial transactions. It is used in maintaining systematic and balanced records of an enterprise's financial transactions. Double entry system follows the fundamental principle that every financial transaction has dual effects on enterprise's accounts. This means that for every debit entry recorded, there must be an equal and corresponding credit entry. Double-entry system provides a more comprehensive view of an enterprise's financial position. It also allows for better analysis and facilitates the preparation of more detailed financial statements.

Single Entry System

Single entry system is sometimes called single entry Book-keeping. It is a simplified Book-keeping method used by small businesses or individuals to track their financial transactions, primarily cash transactions. This is different from double entry system which follows the principle of recording every transaction with at least two entries. Single entry system makes a single entry for each transaction. Single-entry Book-keeping may be simpler and more accessible for small businesses with straightforward financial transactions; the system lacks capacity to deal with records of large entities with varieties of transactions and high volume of trade.

As businesses grow or become more complex, they often change from single-entry system to double-entry system to ensure better financial control and reporting.

Example 2.2

Let say you have a retail shop selling cereals. On 15th September 2023 you sold 10 kilogrammes of rice for TZS 3,000 per kilogramme in cash. 18th September 2023 paid TZS 50,000 as a transport cost for goods purchased. In your single-entry book-keeping system, you would record these transactions as cash inward and outward. You would enter the details as follows:

| Date | Description | Receipts (TZS) | Payment (TZS) |

|---|---|---|---|

| 2023 | |||

| 15/09 | 10 kilogrammes of rice @3,000 | 30,000 | |

| 18/09 | Transport cost | 50,000 |

Characteristics of Single Entry System

These are few examples of characteristics of single-entry system in the recording of financial transactions:

- The level of accuracy on recording financial transactions is different. Single-entry system does not maintain the same level of details and accuracy as double-entry does. It is more straightforward and less comprehensive. Also, it lacks self-checking mechanism in contrast with double entry.

- Every transaction is recorded only once, typically in a simple ledger or journal.

- The main focus is primarily on tracking cashflows, such as receipts and payments.

- The single entry is normally recorded as either a receipt or payment representing an increase or decrease in the cash balance. It would not use two sides to record transactions.

- Single-entry system does not maintain a formal ledger with separate accounts. Instead, it relies on a running total of cash inwards and outwards.

- Financial statements, such as income statements and financial positions, are not readily available with single-entry system.

Activity 2.2

Read more about accounting principles and concepts from various reliable sources, then write short notes, and finally keep your notes in a portfolio for future reference.

Relevance of Accounting Concepts and Principles in Book-Keeping

The relevance of accounting concepts and principles in Book-Keeping is to improve the communication of financial information in language that is acceptable and understandable among enterprises. The principles promote uniformity in the preparation of financial statements, making it possible for persons to compare the financial performance and position of different enterprises. The concepts are there to make financial statements and reports relevant, reliable, and understandable to users of financial information.

Relationship between Accounting Principles and Concepts

None of the accounting concepts presented is expected to be applied in isolation. In many cases, the application of some accounting concepts will reinforce others. A few examples are given to explain such relationships.

Going Concern Principle and the Historical Cost Concept

The assumption of a going concern has an effect on the values of assets and liabilities that are reported in the financial statements. When thinking about the figure to be reported for different assets in the financial statements, a business has to avoid looking at the value such that each asset can be sold in the market at present time. This is because doing so will reflect an assumption that the assets are held for the purpose of being sold rather than for the purpose of being used in a business. Reporting assets at market value would be appropriate when the business is expected to be closed in the near future (That is, within the next 12 months) or the business is no longer a going concern. The historical cost concept makes this possible by prescribing that assets should be reported at their historical cost unless there are reasons to conclude that the business is no longer a going concern.

Going Concern Concept and the Accounting Period Concept

The going concern principle literally assumes no end in the lifespan of a business. It means that one would have to wait up to the end of the business to determine a profit or a loss. Because of the need to know the performance of the business, the life of the business is divided into uniform accounting periods at the end of which financial statements are prepared and presented. In this way, the going concern principle is observed, but without affecting the ability of the business to measure its performance.

Accounting Period Concept and the Matching Principle

As already defined, the accounting period is reflected in the act of dividing the life of a business into a uniform length of accounting periods. It is known that at the end of each period, the performance of the entity is measured by matching revenue and expenses. If there was no uniformity in the period covered by expenses and the one covered by revenue, then there would not be any meaningful profit or loss reported.

Exercise 2.1

Imagine that you are starting a small business selling handmade crafts. Before you begin recording your financial transactions, what are the fundamental principles and concepts of Book-keeping that you think you should be aware of? Use three principles or concepts to explain their functions in recording business transactions.

Summary

This chapter, explored the fundamental principles and concepts of Book-keeping, gaining a solid understanding of the core concepts that form the backbone of financial record-keeping. The following is a summary of the key points in the chapter:

- Double-entry system: The double-entry system is the foundation of Book-keeping, where every financial transaction involves at least two accounts, completing a debit entry and a credit entry. This system ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced, promoting accuracy and integrity to financial records.

- Practical application: Understanding Book-keeping principles is essential for effective financial management in both personal and business contexts. Accurate Book-keeping activities help to monitor cashflow, make informed financial decisions, comply with tax regulations, and evaluate the financial health of an enterprise.

By grasping these basic principles and concepts of Book-keeping, you have equipped with a valuable skillset for managing finances and supporting business growth. Moving forward, you can build upon this foundation, exploring more advanced topics and refining Book-keeping practices to foster financial success and stability.

Revision exercise 2

- Explain the core principle that serves as the basis of Book-keeping, requiring every financial transaction to be recorded with a minimum of two accounts, one debit and one credit.

- Why is understanding of Book-keeping principles important for effective financial management in both personal and business contexts?

- Write a brief note explaining why the double entry system is a cornerstone of Book-keeping.

Chapter Three: Application of the Double Entry System

Introduction

The use of the double entry system requires that every business transaction must be recorded twice in the books of accounts. In this chapter, you will learn accounting equation, statement of affairs and the concept of double entry. The competencies developed will enable you to use double entry principles appropriately on posting the business transactions in the books of accounts.

Think

On the way in which the business should keep record of the machine acquired and cash paid.

Accounting Equation

The accounting equation shows resources owned by a business against those due to others. To understand this equation, think of Habibu, who just started a barber shop business on 1st January 2020. To start this business, he rented a room, bought equipment (shaving machines), furniture (chairs and shelves), fittings (wall fittings and glasses), and consumables (soap, creams and towels). He also had some cash to pay day to day running costs such as electricity, water and repairs. The items needed to start and operate this business (equipment, furniture, fittings, consumables and cash) are called assets.

Assets are resources that an enterprise controls and uses to conduct its business. Also, they include goods kept for sale or consumed in the process of providing services, which are called stock or inventory.

Stock (inventory) are goods which are held by the business for resale, or consumed in the process of providing services. For a manufacturing firm, they may be finished goods, partly finished goods or raw materials awaiting conversion or processing into finished goods which will then be sold.

The question here would be, how did Habibu's business come to have these assets? One of the possible answers is that Habibu saved money from his previous work and decided to invest this money into his business. In this case, the amount that Habibu saved to start the business is referred as capital. Another possibility is that Habibu borrowed money from friends, relatives, banks or other financial institutions to start a business. In this case, the amount borrowed by Habibu as debts is commonly known as liabilities. Capital, also known as owner's equity may thus be defined as amount of resources contributed by the owner to start or expand a business. Assuming that the business starts by owner's resources without any external funding, then the total assets equal the amount of capital, in this case the accounting equation is represented as:

Liabilities arise from having persons other than the owners of the business provide resources to start, expand or run the day-to-day activities of the business. Liabilities are obligations that a business has to settle by means of transferring economic resources to other person(s) or business (es). When a business has resources supplied both by the owner and others who do not own the business, the accounting equation changes to be:

The equation can also be changed or written in words as follows:

(Assets) = (Capital + Liabilities)

Example: Habibu's Business

Assume that the values of each item are as presented below:

Habibu's assets at 1st January 2020

| Item(s) | TZS |

|---|---|

| Shaving machines | 480,000 |

| Furniture | 620,000 |

| Fittings | 216,000 |

| Consumables (soap, creams and towels) | 115,000 |

| Cash | 510,000 |

| Total Assets | 1,941,000 |

To be able to arrive at the accounting equation, you are firstly required to add up all assets. The total obtained by adding up all the listed assets is TZS 1,941,000. Secondly, you were to show the resources that are used in acquiring the assets.

Assume that the business has not taken any liabilities to meet the above costs of resources, then Habibu must be the only source of funding. From these figures, applying the equation ASSETS = CAPITAL, find that Capital = TZS 1,941,000, being the sum of the assets that is, TZS (480,000 + 620,000 + 216,000 + 115,000 + 510,000). This means Habibu supplied TZS 1,941,000 to business and used that amount to start his business.

Assuming that Habibu used own funds to finance the starting of the business, except for the furniture and fittings that were borrowed from Mwakapande, the accounting equation will be shown as follows:

1,941,000 = 1,105,000 + 836,000

Liabilities are composed of the value of borrowed furniture (TZS 620,000), and fittings (TZS 216,000) and capital reflects the amounts paid by Habibu for shaving machines (TZS 480,000), consumables (TZS 115,000) and cash (TZS 510,000).

Types of Book-keeping Accounts

Book-keeping entries are made to reflect effects of transactions of different accounts. These accounts can be further classified according to elements of financial statements which are:

| Element | Description | Examples |

|---|---|---|

| Assets | Resources that a business controls and use in the operations | Cash, trade receivables, inventory, equipment, buildings, and investments |

| Liabilities | What a business owes to others, including debts and obligations | Trade payables, loans payable, accrued expenses, and mortgages |

| Revenue (Income) | Money earned by the business through its normal operations | Sales revenue, service revenue, interest income, and rental income |

| Expenses | Costs incurred by the business in generating revenue | Salaries, rent, utilities, office supplies, advertising expenses, and depreciation |

| Capital | Owner's equity or net worth in the business | Initial capital, additional contributions, retained earnings |

Components of Capital Account

The capital account is a fundamental component of a business's financial accounting, and it represents the owner's equity or net worth in the business. The following are the key components of the capital account:

- Initial capital: The amount of money or assets that the owner(s) initially invested in the business when it was started

- Additional contributions: If the owner(s) inject more money, assets, or value into the business at a later stage

- Net income (net loss): The capital account is affected by the net income or net loss generated by the business

- Drawings or withdrawals: If the owner(s) withdraw funds or assets from the business for personal use

- Retained earnings: The portion of net income that is not distributed to the owner(s) as dividends but is instead reinvested back into the business

The formula to calculate the balance of the capital account is:

Statement of Affairs

Statement of affairs can show the effect of different changes in the accounting equation. It lists the elements of the accounting equation in a systematic manner to show how such equation balances. The statement lists all the assets (with their values) together, and in the same manner lists all items of capital and liabilities.

Statement of affairs: A statement which lists all assets and liabilities (together with their financial value) at a particular date to enable one calculate value of capital.

Habibu's Statement of Affairs as at 1st January 2020

| Details | TZS |

|---|---|

| Assets: | |

| Shaving machines | 480,000 |

| Furniture | 620,000 |

| Fittings | 216,000 |

| Consumables (soap, creams, and towels) | 115,000 |

| Cash | 510,000 |

| Total Assets | 1,941,000 |

| Capital and liabilities: | |

| Liabilities | - |

| Total liabilities | - |

| Capital | 1,941,000 |

| Total capital and liabilities | 1,941,000 |

Concept of Double Entry

The accounting equation is the foundation of the concept of double entry. Double entry deals with the recording and posting of business transactions in the books of accounts. Business transactions are posted to ledger accounts following principle of double entry.

Double Entry System of Book-keeping

Double entry system of Book-keeping records each transaction by making two corresponding entries in the books of accounts. The reason for making two corresponding entries in the books is to simultaneously take into account the two effects of each transaction on the accounting equation. The entries are therefore made so that they cancel each other to reflect the two effects on the accounting equation. By doing this, the accounting equation would balance at any point in time.

Rules for Debit and Credit Entries

| Element | Increases | Decreases |

|---|---|---|

| 1. Assets | Debit | Credit |

| 2. Liabilities | Credit | Debit |

| 3. Capital (owner's equity) | Credit | Debit |

| 4. Revenue (gain) | Credit | Debit |

| 5. Expenses (losses) | Debit | Credit |

Steps for Making Double Entry

What is needed is to:

- Establish the specific items in the elements of accounting equation that are affected by the two effects of the transaction

- Establish the effect, whether it is an increase or decrease in each case

- Make respective entries for recording each effect accordingly

Example 3.1: Applying the Double Entry Rules

Take an example of the following transactions conducted by Habibu's business:

- Paid cash TZS 25,000 on 31st January in respect of electricity bill for the month.

- Received TZS 20,000 from a customer for a haircut of her four children.

Solution:

For transaction 1:

The transaction involves an increase in expenses (electricity) by TZS 25,000 and a decrease in asset (cash) by TZS 25,000.

Debit: Electricity expense TZS 25,000

Credit: Cash TZS 25,000

For transaction 2:

The transaction involves an increase in asset (cash) by TZS 20,000 and an increase in revenue by TZS 20,000.

Debit: Cash TZS 20,000

Credit: Service revenue TZS 20,000

Steps for Identifying and Posting Transactions

Steps to be followed when identifying and posting transactions in the ledger accounts:

- Step 1: In each transaction, identify two accounts involved in the transaction

- Step 2: Find out the element to which each of the accounts involved belong

- Step 3: Indicate the effect of transaction (increase or decrease)

- Step 4: Debit and credit appropriate ledger accounts by applying the rules of double entry

Example 3.2: Identifying Accounts and Effects

For each of the following transactions below, identify two accounts involved, their types, and state which account should be debited and which one should be credited.

| Date | Transaction | Accounts Involved | Element | Effect | Debit/Credit |

|---|---|---|---|---|---|

| 2020 Jan 1 | Diana started a business by depositing TZS 2,000,000 capital in the bank account | Bank account, Capital account | Asset, Capital/equity | Increase, Increase | Debit, Credit |

| Jan 4 | Bought machinery worth TZS 200,000 on credit from Alpha | Machinery account, Alpha account | Asset, Liability | Increase, Increase | Debit, Credit |

| Jan 8 | Purchased goods worth TZS 400,000 on credit from Julius | Purchases account, Julius account | Expense, Liability | Increase, Increase | Debit, Credit |

| Jan 12 | Sold goods for cash TZS 150,000 | Cash account, Sales account | Asset, Revenue | Increase, Increase | Debit, Credit |

Importance of Double Entry

The use of the double entry system is important in accounting process due to the following reasons:

- Makes it easier to show the two effects of each transaction: The double entry system requires every transaction to be recorded twice, making it easier to understand which accounts have been affected

- Assures arithmetic accuracy in the accounts thus minimising the possibility of errors: Since every debit must have a corresponding credit entry, arithmetic accuracy is assured

- The basis of the balances used in preparing the financial statements: Balances used in preparing trial balance and financial statements are extracted from ledger accounts following double entry system

- Ensures that financial records are kept properly: Double entry ensures that financial records are kept permanently and properly in the books of accounts

Activity 3.2

Your friend, Zawadi has approached you to clarify an important aspect in Book-keeping. She has heard you speaking about double entry, and she believes that the use of double entry will:

- Double the work of the book-keeper and thus, spend more resources of the enterprise

- Encourage recording transactions twice, which is misleading as it doubles the amounts reported; thus, some kind of cheating may occur

Prepare a short presentation that you will use to explain to her the double entry system and show its benefits to the enterprise.

Summary

The principle of double entry is a fundamental concept in accounting and book-keeping. It ensures that every financial transaction has an equal and opposite effect on at least two accounts. This system is widely used in maintaining accurate and balanced financial records. By following the double entry system, businesses can achieve logically organised records that can be used in preparing financial statements. This, in turn, enables them to analyse their financial performance, financial position and cashflow make informed decisions, and meet reporting requirements. The application of the principle of double entry provides a strong and consistent framework for recording financial transactions, helping businesses to maintain a clear and accurate representation of their financial activities and facilitating effective financial management.

Revision Exercise 3

- Complete the gaps in the following table:

Assets TZS Liabilities TZS Capital TZS (a) 1,650,000 507,000 ? (b) ? 516,000 1,032,000 (c) 1,083,000 ? 855,000 - Complete the columns to show the effects of the following transactions by inserting a (+) sign for the increase and a (-) sign for the decrease

- From the following items below, identify which ones are assets and which ones are liabilities

- Classify the following items into liabilities and assets

- Complete the following table by showing the effects, the account to be debited, and the account to be credited

Chapter Four: Recording of Business Transactions

Introduction

Recording of transactions in the books of accounts is the initial and very critical stage in accounting. Correctness of the first record (prime or original) in the books of accounts for a transaction is the basis for having appropriate accounting records. In this chapter, you will learn books of prime entry and preparation of such books. The competencies developed will enable you to prepare books of prime entry according to the required principles.

Think

Operating a business without recording its financial transactions.

Books of Prime Entry

Books of prime entry, also known as books of original entry or daybooks, form an essential part of the double-entry accounting system used by businesses to record their financial transactions. These books serve as the first point of entry for all the business transactions before they are posted into the ledger or processed further towards preparation of financial statements. The use of books of prime entry ensures that transactions are recorded promptly and accurately, minimising the risk of errors and providing a comprehensive record of financial activities. Daybooks are the principal sources of transactions posted into the general ledger, which ultimately lead to the preparation of financial statements. Overall, books of prime entry play a crucial role in maintaining an efficient and organised accounting system for any business.

Meaning of Books of Prime Entry

Books of prime entry (journals) are the books of accounts that are used to record any transaction for the first time. In the books of prime entry, each transaction is recorded with as much detail as possible, in order to provide information concerning the transaction. The name journal is adopted from a French word for diary. It is therefore, a good practice to record transactions in the books of prime entry in a chronological order. Transactions are also recorded as soon as possible from the time they occur to avoid situations where they may be forgotten or have their source documents misplaced.

Types of Books of Prime Entry

Books of prime entry are also known as journals or day books, except for a cash book. These books are commonly termed as special journals or daybooks because they are used to record transactions of specific type on the daily basis. There are six types of books of prime entry as presented below:

- Sales journal (sales daybook)

- Purchases journal (purchases daybook)

- Sales returns journal (sales returns daybook)

- Purchase returns journal (purchase returns daybook)

- Cash book

- General journal (journal proper)

Use of Books of Prime Entry

As their names suggest, each book serves its own purpose:

| Book | Purpose |

|---|---|

| Purchases daybook | Used to record transactions related to credit purchases of goods |

| Sales daybook | Used to record transactions related to credit sales of goods |

| Sales returns daybook | Used to record details of transactions related to sales returns from customers |

| Purchase returns daybook | Used to record transactions related to purchase returns to suppliers |

| Cash book | Used to record transactions related to receipt and payment of cash as well as bank transactions |

| General journal | Used to record transactions related to other items not recorded in special journals |

Source Documents

The information recorded in the books of original entry is taken straight from the documents that may either have been issued by the business or by its suppliers. These documents are called source documents, because they are the source of information for recording transactions in the books.

Common Source Documents

Cash Receipt Voucher

Company name and address

Voucher Number: ...... Date: ......

| S/N | DESCRIPTION | UNIT PRICE | QUANTITY | AMOUNT (TZS) |

|---|---|---|---|---|

TOTAL

Amounts in words: ......

Cash/ Cheque Number ......

Received by: ...... Signature ...... Date: ......

Activity 4.1

Prepare a sample of cash receipt voucher and demonstrate how to fill it out.

Payment Voucher

Company name and address

PV No: ______

Amount: ______ Date: ______

Method of Payment

Cash: ______ Cheque: ______

To: ______

The Sum of:

Being: ________________________

Payee: _______________________

Approved By: ___________ Paid By: ___________ Signature ___________

Invoice

Company Name

Address ________________________ Date ________________

Phone No 1 +255-000-000-000

Phone No 2 +255-000-000-000

Fax +255-000-000-000

Email sales@enterprise.com

website www.enterprise.com

Bill To:

Name ________________________

Address ______________________

Tin No _______________________

Phone No _____________________

| S/N | DESCRIPTION | UNIT PRICE | QUANTITY | AMOUNT (TZS) |

|---|---|---|---|---|

Subtotal _______ Taxable _______ Tax rate (18%) _______ Tax due _______ TOTAL _______

Preparation of Books of Prime Entry

As per the accounting cycle or process introduced in chapter one; once transactions are identified, they are entered in the books of prime entry, followed by posting the entries to relevant ledger accounts.

Purchases Daybook or Purchases Journal

When goods are purchased on credit, the seller will prepare and send an invoice to the buyer. The buyer will record this transaction in the purchases daybook because the transaction involves a credit purchases, meaning that the buyer did not pay for the goods at the time of purchase.

Example 4.1

Record the following transactions in the purchases daybook for the month of July 2023.

2023 July 1 Bought from Tom Ltd. invoice number 043516:

10 bags of rice, each with 5kgs @ TZS 10,000

20 bags of sugar, each with 5kgs @ TZS. 15,000

July 9 Bought from Asha invoice number 03167:

10 boxes of pens @ TZS 2,000

5 cartons of ruled papers @ TZS 30,000

July 16 Bought goods from Katabo for TZS 60,800 invoice number 06312

July 29 Bought from Mwanaidi, invoice number 09842:

15 pairs of sandals @ TZS 15,000

14 boxes of kids drawing pens @ TZS 5,000

Solution

10 bags of rice(5kgs) @ TZS 10,000

20 bags of sugar (5kgs) @ TZS 15,000

300,000

10 boxes of pens @ TZS 2,000

5 cartons of ruled paper @ TZS 30,000

150,000

Goods

15 pairs of sandals @ TZS 15,000

14 boxes of kids drawing pens @ TZS 5,000

70,000

Sales Daybook or Sales Journal